China promotes the high-quality development of the capital market, plays a "combination boxing" and presses the "acceleration button" for Chinese modernization.

CCTV News:The Opinions on Strengthening Supervision, Preventing Risks and Promoting the High-quality Development of the Capital Market issued on April 12 clearly put forward that we should vigorously promote the medium and long-term capital to enter the market and continue to expand the long-term investment power. China Securities Regulatory Commission (CSRC) said that it is working with relevant authorities to study and formulate specific measures to guide all kinds of medium and long-term funds to increase the scale of equity investment.

Shen Bing, director of the Department of Securities Fund Institution Supervision of China Securities Regulatory Commission, said that the specific measures include actively promoting the long-term stock investment pilot of insurance funds and improving the stability and investment scale of stock investment of insurance funds. Further improve the stock investment policies of the national social security fund and the basic old-age insurance fund. Improve the flexibility of enterprise annuity and personal pension investment.

By the end of last year, the market value of A-shares held by various professional institutional investors totaled 16 trillion yuan, more than doubling in five years, and the shareholding ratio increased from 17% to 23%. Among them, Public Offering of Fund holds the A-share market value of 5.1 trillion yuan, and its shareholding ratio has increased from 4% to 7.3%, making it the largest professional institutional investor in the A-share market.

China Securities Regulatory Commission: It is planned to moderately increase the financial indicators of listing on the Main Board and Growth Enterprise Market.

The Opinions on Strengthening Supervision, Preventing Risks and Promoting the High-quality Development of the Capital Market issued on April 12th also proposed to raise the listing standards of the Main Board and the Growth Enterprise Market. China Securities Regulatory Commission said that improving the financial indicators of listing on the Main Board and Growth Enterprise Market is the need to improve the quality of listed companies from the source, better protect the interests of investors and serve the high-quality development of the economy.

Yan Bojin, chief risk officer and director of the issuance department of China Securities Regulatory Commission, said that it is planned to moderately increase the financial indicators of listed companies on the main board and the Growth Enterprise Market. For the last year, the net profit indicators of the main board and the Growth Enterprise Market are planned to be raised to 100 million yuan and 60 million yuan respectively. The financial conditions for the listing of enterprises in science and technology innovation board and Beijing Stock Exchange remain unchanged, but higher requirements are proposed for the scientific and technological attributes of enterprises in science and technology innovation board.

Yan Bojin said: "With this arrangement, the sectors can be stepped up, and the levels of the sectors are more distinct and the characteristics are more prominent, which can better meet the needs of enterprises with different development stages, different industry attributes and different business scales, and also better meet the needs of investors with different investment purposes and various risk preferences."

China Securities Regulatory Commission issued "Opinions on Strictly Implementing the Delisting System": deepening the system reform and strictly enforcing a number of delisting standards.

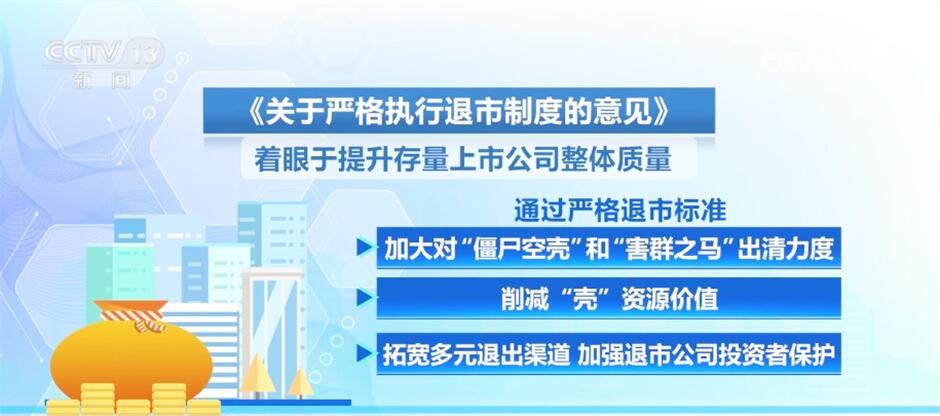

On April 12th, China Securities Regulatory Commission issued the Opinions on Strictly Implementing the Delisting System (hereinafter referred to as the Delisting Opinions) to further deepen the reform of the delisting system.

The Delisting Opinions focuses on improving the overall quality of listed companies in stock. Through strict delisting standards, we will intensify efforts to clean up "zombie empty shells" and "black sheep" and reduce the value of "shells" resources. At the same time, broaden diversified exit channels and strengthen investor protection of delisting companies.

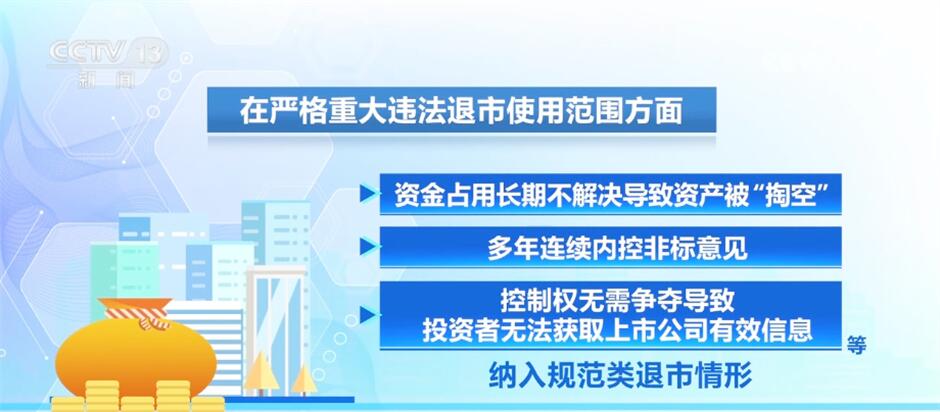

In terms of strict scope of application of serious illegal delisting: lowering the threshold for two years of financial fraud to trigger serious illegal delisting, and adding one year of serious fraud and years of continuous fraud delisting. The long-term unresolved occupation of funds leads to the "hollowing out" of assets, years of continuous internal control and non-standard opinions, and disorderly competition for control rights leads to the inability of investors to obtain effective information of listed companies, which are included in the normative delisting situation. In addition, it also includes measures such as improving the operating income delisting index of loss-making companies and improving the market value standard and other trading delisting indicators.

In terms of further unblocking multiple delisting channels: improve policies and regulations such as absorption and merger, and encourage and guide head companies to increase their efforts to industry consolidation based on their main business.

In terms of weakening the value of "shell" resources: strengthen the supervision of mergers and acquisitions, strengthen the relevance of the main business, and strengthen the supervision of "backdoor listing". Strengthen the supervision of acquisition, compact the responsibility of intermediaries, and standardize the transaction of control rights. Strictly crack down on illegal activities behind "shell speculation". Resolutely identify listed companies that have no reorganization value.

In addition, the "Delisting Opinions" also made detailed requirements for strengthening delisting supervision and implementing compensation and relief for delisting investors. The China Securities Regulatory Commission said that the next step will be to promote all measures as soon as possible, crack down on all kinds of delisting evasion, protect the rights and interests of investors, improve the quality of listed companies and purify the ecology of the capital market.

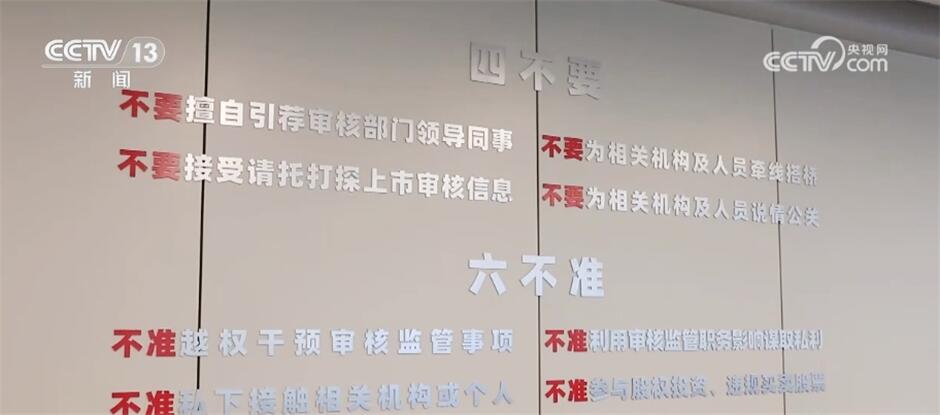

The China Securities Regulatory Commission publicly solicited opinions on six draft rules such as issuance supervision

On the 12th, the China Securities Regulatory Commission publicly solicited opinions on six draft rules concerning issuance supervision, supervision of listed companies, supervision of securities companies and supervision of transactions.

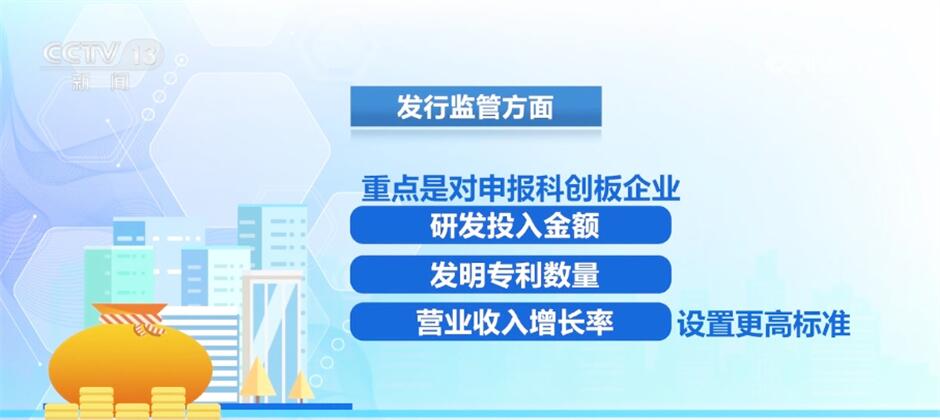

In the aspect of issuance supervision, the focus is to set higher standards for the amount of R&D investment, the number of invention patents and the growth rate of operating income of science and technology innovation board enterprises. At the same time, the proportion of random inspection of starting enterprises will be greatly increased from 5% to 20%, and the proportion of problem-oriented on-site inspection and on-site supervision of the exchange will be increased accordingly. After adjustment, the overall proportion of on-site inspection and supervision will not be less than one third.

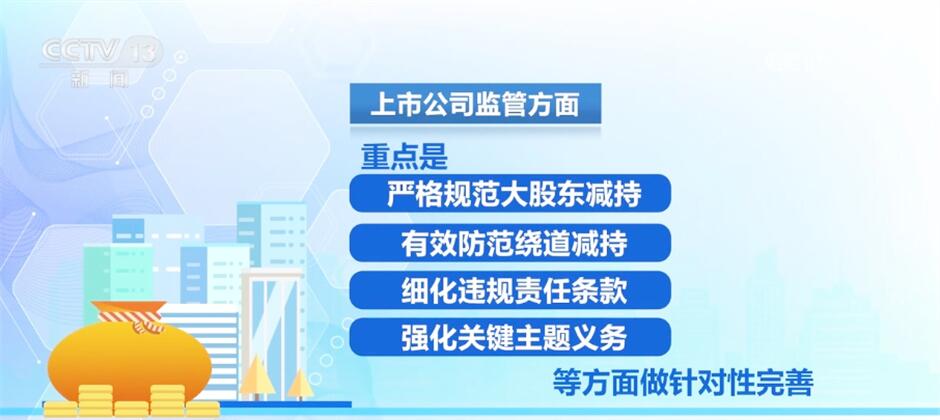

In terms of supervision of listed companies, the key points are to strictly regulate the reduction of major shareholders, effectively prevent the reduction of detours, refine the liability clauses for violations, and strengthen the obligations of key subjects. At the same time, it absorbs and integrates the requirements of the original reduction regulations on regulating Dong Jiangao’s reduction of shares, and further clearly stipulates that all parties shall abide by the original reduction restrictions after divorce and share splitting.

In the aspect of securities company supervision, the key point is to urge the company to correct its business philosophy and focus on its main business; Strengthen internal checks and balances, strengthen the control of domestic and foreign subsidiaries; Strengthen the information disclosure of risk control indicators and carry out financing reasonably and prudently.

In terms of transaction supervision, the key points are to clarify seven contents, such as programmed transaction, transaction monitoring and risk prevention and control, and high-frequency transaction supervision. In addition, the Shanghai and Shenzhen Stock Exchanges simultaneously solicited opinions from the public on 19 specific business rules such as stock issuance and listing review and listing rules, involving improving listing conditions, standardizing the reduction of holdings, and strictly delisting standards.

The China Securities Regulatory Commission publicly solicited opinions on standardizing programmatic transactions: compacting the responsibility of brokers and drawing a "red line" for trading behavior

On the 12th, the China Securities Regulatory Commission issued the Provisions on the Management of Programmatic Trading in the Securities Market (Trial) (Draft for Comment). Among them, it is proposed to tighten the management responsibility of brokers to customers, set monitoring indicators for abnormal transactions, draw a "red line" for trading behavior, standardize the management of technical systems, and clarify the technical system requirements of investors and securities companies.

Zhang Wangjun, Director of Market Supervision Division I of China Securities Regulatory Commission, said that the procedural transaction management regulations for public consultation closely focus on the main line of strengthening supervision, preventing risks and promoting high-quality development, and adhere to the idea of "pursuing advantages and avoiding disadvantages, emphasizing fairness, effective supervision and standardized development", further making comprehensive and systematic regulations on procedural transaction supervision, and effectively improving the pertinence and effectiveness of procedural transaction supervision.

According to Zhang Wangjun, from the content point of view, the opinions mainly highlight the maintenance of fairness, full chain supervision, system policy, etc. At the same time, it is required that the stock exchange clarify the identification standards for high-frequency transactions, and can implement differentiated charges for high-frequency transactions and strictly manage their abnormal trading behavior.

In recent years, China Securities Regulatory Commission continued to explore and improve the regulatory mechanism of programmed transactions. In September 2023, China Securities Regulatory Commission directed the stock exchange to establish a programmed transaction reporting system. By the end of 2023, the whole market had reported 119,000 programmed trading accounts, which has achieved "all reports should be made". In February this year, the China Securities Regulatory Commission instructed the Shanghai and Shenzhen Stock Exchanges to take timely regulatory measures against abnormal trading behaviors of individual quantitative institutions.